The German event industry, a cornerstone of the nation’s service economy and a vital driver for the trade fair and tourism sectors, is currently navigating a complex financial landscape characterized by long-term stability and emerging liquidity bottlenecks. A comprehensive analysis recently released by Creditsafe Deutschland, the world’s most frequently utilized business credit information provider, in collaboration with the industry portal eventcompanies.de, highlights a sector that is fundamentally robust but increasingly bifurcated. While nearly three-quarters of the companies within this ecosystem maintain solid credit ratings, a concerning trend is emerging among event locations and specific service providers, where rising fixed costs and delayed payment cycles are beginning to strain the "pre-performance" chain that defines the industry.

As of mid-March 2026, the data indicates that the event industry remains a sector defined by maturity and experience rather than rapid, disruptive growth. The inherent structure of the business—where technical services, stage construction, and personnel must be secured and paid for long before the final invoice is settled—creates a unique financial pressure cooker. This "pre-performance" model means that the solvency of a single partner, particularly those at the top of the project chain such as venues or lead agencies, can dictate the financial health of dozens of subcontractors.

The Structural Backbone: Maturity and the SME Landscape

One of the most striking revelations from the Creditsafe report is the sheer longevity of the players involved in the German event market. According to the data, 74.9 percent of all active event companies have been in operation for more than 15 years. In contrast, the rate of new market entrants—companies aged between zero and one year—stands at a negligible 0.3 percent.

Industry consultant Klaus Grimmer, owner of kg-u (Klaus Grimmer Unternehmens- und Personalberatung) and a veteran advisor with over two decades of experience, suggests that this demographic profile is a direct reflection of the "trust economy" that governs the sector. In an environment where a single technical failure or logistical delay can result in millions of euros in losses, clients and lead contractors gravitate toward established names with proven track records. Growth in this sector is rarely fueled by aggressive startups; instead, it is built through the slow accumulation of reference projects, the refinement of operational routines, and the cultivation of resilient partner networks.

This maturity is most pronounced among service providers and trade fair construction firms (Messebau), where 80.1 percent and 78.4 percent of companies, respectively, have surpassed the 15-year milestone. This longevity provides a stabilizing effect on the market, as these firms have historically demonstrated the ability to weather economic cycles, including the volatile recovery period of the early 2020s. However, the low rate of new foundations also suggests a potential "innovation trap," where professionalization and incremental process improvements within existing firms take precedence over radical market disruption.

Creditworthiness and the "Location Gap"

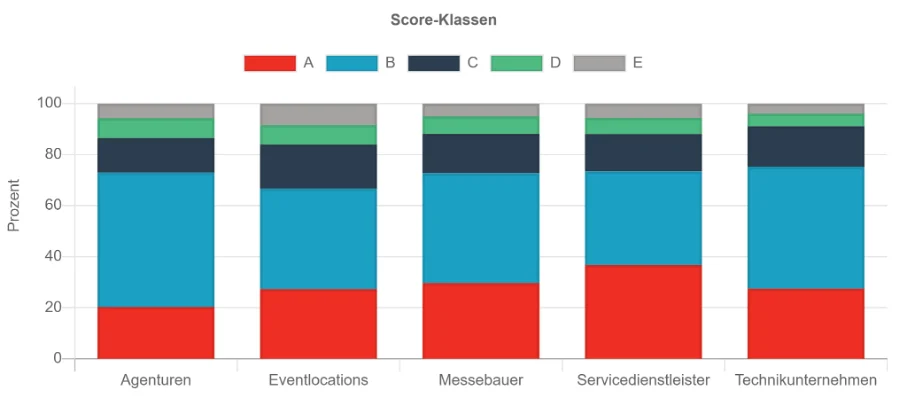

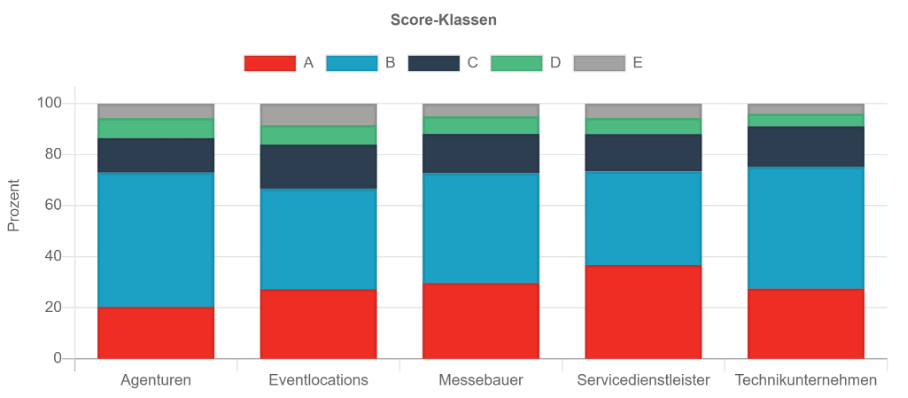

The overall credit landscape of the German event industry appears healthy on the surface, with 72.2 percent of companies falling into the top-tier "A" and "B" score classes. Specifically, 28.1 percent of firms boast an "A" rating (representing a very low risk of default), while 44.1 percent hold a "B" rating.

The service provider segment leads the pack in terms of financial excellence, with 36.7 percent achieving the highest possible credit score. Analysts attribute this to more professionalized corporate structures, diversified client portfolios, and a more disciplined approach to risk management following the global supply chain disruptions of previous years.

However, the report identifies a significant "problem field" within the event location segment. Venues and event spaces show a disproportionately high concentration in the weaker "D" and "E" score classes, which represent a high to very high risk of insolvency. Approximately 16.1 percent of locations currently occupy these precarious categories.

The economic logic behind this disparity is rooted in the high fixed-cost nature of physical venues. Unlike technical service providers or agencies that can scale their freelance workforce or equipment rentals based on demand, locations are burdened with permanent overheads: long-term leases or mortgages, energy costs for massive climate-controlled spaces, and permanent facility management staff. When bookings fluctuate due to seasonal shifts, corporate budget freezes, or short-term cancellations, these fixed costs continue to accrue, rapidly eroding liquidity and negatively impacting credit scores.

Payment Morality: The Domino Effect of Delayed Cash Flows

Perhaps the most critical indicator for subcontractors and freelancers is the industry’s payment behavior. The Creditsafe analysis reveals that, on average, only 45.2 percent of companies in the event sector pay their invoices within the agreed-upon terms. While agencies, trade fair builders, and technical firms perform better than the average—with on-time payment rates between 57 and 59 percent—the bottlenecks at the "knots" of the project chain are severe.

For event locations and specific service segments, more than 23 percent of companies are reporting payment delays exceeding 16 days. In a sector where small and medium-sized enterprises (SMEs) make up 92.5 percent of the market, such delays can be catastrophic. A technical firm that has already paid its crew and rented specialized lighting rigs relies entirely on the prompt settlement of the final invoice to maintain its own working capital.

Klaus Grimmer warns that relying on "old-school" business relationships without verifying current financial data is a high-risk strategy in 2026. He notes that even long-standing partners can experience sudden shifts in their financial stability due to external factors like rising interest rates or shifts in corporate procurement policies. A single large-scale project failure caused by a non-paying location or lead agency can trigger a "domino effect," forcing otherwise healthy subcontractors into their own liquidity crises.

Credit Limits and the Scale of Operations

The financial capacity of the industry is further illuminated by the distribution of credit limits. The majority of the sector—61.6 percent—operates within a credit limit of under 50,000 euros, reinforcing the small-scale, SME-dominated nature of the business.

However, there is a substantial "upper class" of firms capable of handling massive project volumes. Roughly 13.1 percent of companies have credit limits exceeding 250,000 euros, and a select 3.2 percent command limits of over 1 million euros. These high-limit firms are typically the "integrators"—large-scale technical production houses or international service conglomerates that handle multiple major events simultaneously.

The service provider segment again shows higher-than-average resilience here, with 22.1 percent of firms possessing credit limits above 250,000 euros. This financial "buffer" allows these companies to absorb the shocks of delayed payments more effectively than smaller boutique agencies, though it also means they are carrying significantly higher levels of debt and financial risk at any given time.

Market Evolution: Trends Since January 2025

A chronological look at the data since the beginning of 2025 suggests a market in a state of high flux but with a slight upward trajectory. Since January 2025, 43.7 percent of event companies have seen an improvement in their credit scores, while 39.4 percent have experienced a decline. Only 16.9 percent of companies remained stable.

This volatility reflects the extreme sensitivity of the event industry to broader economic indicators such as consumer confidence, corporate investment cycles, and inflation. The "post-pandemic" era has transitioned into an "efficiency era," where companies that have invested in automated Forderungsmanagement (receivables management) and rigorous cost control are pulling ahead, while those clinging to traditional, less transparent business models are losing ground.

The National Focus of a Global Hub

Despite Germany’s status as a global leader in trade fairs and international conferences, the Creditsafe data shows that the provider landscape remains overwhelmingly national. Only 3.2 percent of companies are the subject of credit inquiries from abroad. International business relationships are largely confined to neighboring European countries, the United Kingdom, and the United States.

This domestic focus means that the stability of the German event industry is inextricably linked to the health of the German domestic economy. While this protects the sector from some global geopolitical shocks, it also means that a downturn in German industrial production or a contraction in the national marketing budgets of DAX-listed companies is felt immediately across the entire event supply chain.

Conclusion: Professional Risk Management as a Competitive Necessity

The findings from Creditsafe and eventcompanies.de present a clear mandate for the industry as it moves through 2026: transparency must replace "gut feeling." The solid core of the industry—the 72.2 percent in high-score classes—provides a foundation for optimism, but the pockets of risk in the location and service sectors cannot be ignored.

For agencies, technical firms, and freelancers, the message is one of professionalization. The era of the "handshake deal" as the sole basis for multi-million-euro projects is ending. In an industry where the work is done upfront and the payment comes last, the ability to assess a partner’s creditworthiness is no longer just an administrative task; it is a vital component of project success.

As Klaus Grimmer concludes, the event industry will always be driven by creativity, emotion, and the pursuit of the "perfect moment." However, without the "hygiene" of financial transparency and active risk management, those moments of creativity remain built on a fragile foundation. For the German event industry to maintain its global reputation for excellence, its financial discipline must now match its operational precision. Information, verification, and security are no longer optional—they are the new industry standards for a sustainable future.